The Crack in the Job Market Just Changed Everything for Gold | Global Signal™ — Bullion Intelligence

Gold just finished its worst quarter since 2013. Then the June jobs report came in shockingly weak — and everything that’s been holding gold down started to lift.

For three months, this letter has been telling you the same thing about gold’s decline: it was being driven by two temporary forces — a hawkish Federal Reserve and a soaring dollar — and that when those forces faded, the price would follow the fundamentals back up. This week, for the first time, we got real evidence that the fading has begun. And it came from an unexpected place: the job market.

Let me set the scene, because the turn this week only makes sense against how bad the quarter was. Gold just closed out its worst quarter since 2013. From its January peak near $5,595 an ounce, it fell all the way below $4,000 in late June — a drop of roughly 28% at the lows — as new Fed chairman Kevin Warsh came in tougher on inflation than anyone expected and the dollar climbed to a 14-month high. Silver was hit even harder, falling below $60 and spending weeks pinned there. If you held metal through the spring, this was a genuinely painful stretch, and I’m not going to pretend otherwise.

Then two things happened in the space of 48 hours that started to change the picture.

First, on Wednesday, Warsh gave a speech in Portugal that markets read as a real softening. He noted that the Fed’s preferred underlying inflation measure — the trimmed-mean PCE — has now fallen year-over-year for 36 straight months, which is a quiet way of saying the inflation fight may be closer to won than the headlines suggest. Gold jumped over 2% and silver surged nearly 4% on the day, their best session in weeks, as the dollar pulled back from its highs.

Then, on Thursday, the June jobs report landed — and it was a shock. The economy added just 57,000 jobs, against expectations of 110,000, the weakest in four months. Worse, the prior two months were revised down by a combined 74,000. After three straight months of a red-hot labor market that kept the Fed aggressive and gold suppressed, the job market suddenly looks like it’s cracking. And a cracking job market is exactly the thing that forces the Fed to stop worrying about inflation and start worrying about the economy — which is precisely the shift gold has been waiting for.

This is an in-depth issue, because this is a genuine inflection point and it deserves the full treatment. Let me walk you through what happened, why the jobs report matters so much, where silver’s extraordinary setup stands, what the world’s central banks just told us, and how a patient holder should think about this moment.

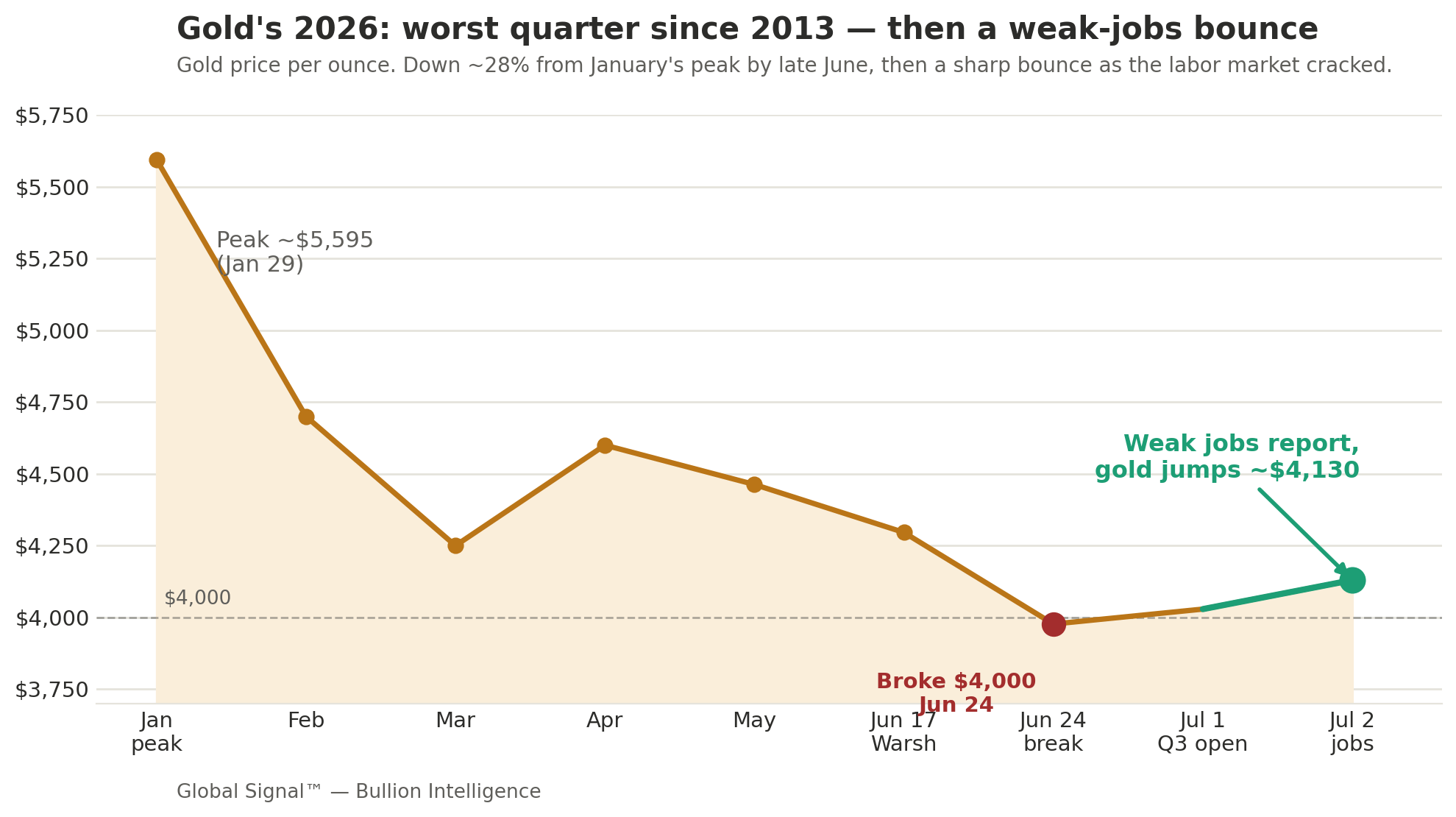

The Picture in One Chart

The chart above tells the whole story of gold’s 2026. The peak near $5,595 in late January. The long, grinding decline through the spring as the Iran war drove up inflation and Warsh’s Fed turned hawkish. The break below $4,000 in late June — that red dot, the worst quarter since 2013. And then, at the very end, the green dot: gold jumping back toward $4,130 as the job market cracked and the rate-hike fears began to lift. That last move is small on the chart, but it may be the most important turn of the year, because of what caused it.

Opening Signal

Here’s the single most important thing to understand this week: the force that has been crushing gold all year just started to reverse, and it reversed for a reason that tends to last.

All year, gold’s enemy has been the fear of higher interest rates. When the Fed is hawkish and rates are high or rising, gold — which pays no interest — becomes less attractive next to a Treasury bond or a savings account, and the dollar strengthens, which pushes gold down further. That’s the machine that drove gold from $5,595 to below $4,000.

What breaks that machine is a weakening economy, because a weakening economy forces the Fed to stop raising rates and start thinking about cutting them. And this week, for the first time all year, the economy flashed real weakness: 57,000 jobs when 110,000 were expected, with prior months revised sharply lower. The market’s response was immediate and telling — traders pushed their bets for the next rate hike from September all the way out to December, and some began questioning whether the Fed will hike at all. The dollar fell. Gold rose. This is the machine starting to run in reverse.

The reason this matters more than a normal up-day is that it’s fundamental, not technical. Gold didn’t bounce because of a chart pattern or a headline. It bounced because the underlying economic story that justifies its decline is beginning to change. That’s the kind of turn that can mark a bottom.

Executive Signal — Premium

The hawkish-Fed headwind is finally starting to lift, and that’s the quarter’s most important development. For three months, the single biggest force pushing gold down was the expectation of Federal Reserve rate hikes, cemented by Warsh’s hawkish debut and a string of hot economic data. This week that expectation cracked. Warsh’s Sintra speech acknowledged that underlying inflation has been falling for 36 straight months, and the shockingly weak June jobs report (57,000 versus 110,000 expected, with 74,000 in downward revisions to prior months) forced markets to push rate-hike bets from September to December. The dollar fell from its 14-month high. This is the exact catalyst gold has been waiting for, and it’s arriving just as the metal sits at its most oversold levels of the cycle.

The quarter was genuinely brutal, and honesty requires naming it. Gold fell roughly 28% from its January peak to its late-June low, its worst quarter since 2013, driven by the hawkish Fed and a dollar surge. Silver fell even harder, breaking below $60 for the first time since December and staying there. Several Wall Street banks cut their near-term targets. This was the deepest drawdown of the entire cycle, and anyone holding metal felt it. The turn this week is meaningful, but it’s the first turn, not a confirmed trend — a genuine bottom takes time to build and confirm.

The structural floor was reconfirmed at the exact bottom, which is the pattern that matters. As gold broke below $4,000, the World Gold Council’s annual survey landed with a striking message: 89% of central banks expect global gold reserves to keep rising over the next year, and a record share plan to add to their own holdings. China’s gold imports tripled in Q1 to 317 tonnes, and the People’s Bank of China ramped its reported buying to eight tonnes in April. The most patient, most informed buyers on earth used this weakness to accumulate — the same pattern we’ve documented all cycle. The paper price fell; the physical floor got stronger.

Silver’s setup is the most compelling in the entire metals complex, and it just got a catalyst. Silver fell harder than gold during the correction, pushing the gold-to-silver ratio up toward 67, but it’s now in its sixth consecutive year of supply deficit, with total supply at a decade high yet demand still outpacing it. When the monetary headwind eased this week, silver immediately outran gold — up 3.75% versus gold’s 2.27% on Warsh’s speech — exactly as it tends to do when rate fears fade. A structurally undersupplied metal at a deep discount, catching a monetary tailwind, is the highest-conviction setup we’ve covered.

For the patient holder, this is the moment the thesis has been building toward. The temporary forces that drove the correction are fading, the structural floor is confirmed at record-strong levels, silver offers the deeper value, and the every-major-bank year-end targets ($4,900 to $6,000) sit far above today’s price. The turn isn’t confirmed yet, but the evidence that it’s beginning is now real rather than hoped-for.

Key Signals at a Glance — Premium

The June jobs report shocked: just 57,000 jobs added vs. 110,000 expected, the weakest in four months, with prior months revised down 74,000. The labor market is visibly cooling for the first time this year.

Gold jumped to ~$4,130 (+2.27%) and silver to ~$61.73 (+3.75%) on the week’s turn, their best session in weeks, as the dollar fell from a 14-month high and rate-hike bets moved from September to December.

The trigger was two-fold: Warsh’s Sintra speech noting the Fed’s trimmed-mean PCE has fallen year-over-year for 36 straight months, plus the weak jobs data — together easing the hawkish-Fed headwind that drove the correction.

The quarter was gold’s worst since 2013 — down ~28% from the January peak of $5,595 to below $4,000 in late June. Silver fell even harder, below $60 for the first time since December.

The structural floor reconfirmed at the bottom: 89% of central banks expect global reserves to rise, a record share plan to add, and China’s Q1 gold imports tripled to 317 tonnes.

Silver’s setup stands out: 6th straight year of supply deficit, decade-high demand, and it outran gold on the turn — the classic pattern when monetary headwinds ease. Every major bank’s year-end gold target ($4,900–$6,000) sits far above spot.

The real positioning map starts below →

Conviction map, named vehicles for each thesis, forward scenarios with confidence tiers, the Cycle & Cosmos read, and the Watch Triggers for the weeks ahead — in the Premium Subscription. Premium subscribers see this on publish day. Free subscribers receive it 7 days later.