Gold Rallied on Good News, Then Gave It All Back. The Reason Matters. | Global Signal™ — Bullion Intelligence

Inflation cooled, gold jumped $90, and then it surrendered the gains within two days. The explanation reveals exactly what’s holding this market hostage — and where the real opportunity is hiding.

Last week I explained why gold had been falling on news that should have lifted it — because in 2026, gold trades on interest rates, not fear, and the war was pushing rates the wrong way. This week gave us the mirror image of that lesson, and it’s just as important to understand.

Here’s what happened. On Tuesday, the June inflation report came out, and it was genuinely good news. Headline inflation dropped to 3.5%, well below the 3.8% expected, with the steepest monthly decline since April 2020. Core inflation cooled to 2.6%. This was exactly what gold had been waiting for — softer inflation means less pressure on the Fed to raise rates, which means lower real yields, which is fuel for gold. And gold responded immediately, jumping about $90 to roughly $4,089, with silver popping too. For a day, it looked like the turn was finally here.

Then, over the next two days, gold gave almost all of it back. By Friday it had slid back toward $4,000, and silver had dropped to around $56. The good inflation news didn’t hold. And the reason it didn’t hold is the single most important thing for you to understand about this market right now, because it’s subtle and almost nobody is explaining it clearly.

The June inflation report told us about the past — it measured prices in June, when oil was cheap. But this week, oil was anything but cheap. The Iran conflict escalated again, with the US reinstating a naval blockade on Iranian shipping and reasserting control over the Strait of Hormuz, and oil climbed hard, with Brent pushing toward $87. So the market did something sophisticated: it looked at June’s good inflation number, then looked at July’s rising oil, and concluded that next month’s inflation is going to be worse. The market is now pricing forward inflation faster than the Fed can act on last month’s data. Gold rallied on the backward-looking good news, then surrendered the gains to the forward-looking bad news.

That tension — between what inflation was and what it’s about to become — is what’s holding gold hostage this summer. Let me walk you through it fully: why the rally faded, why silver just hit a genuinely remarkable level of cheapness, what China did again this month that tells you everything about the long game, and how a patient holder should think about a market caught between a cooling past and a heating future.

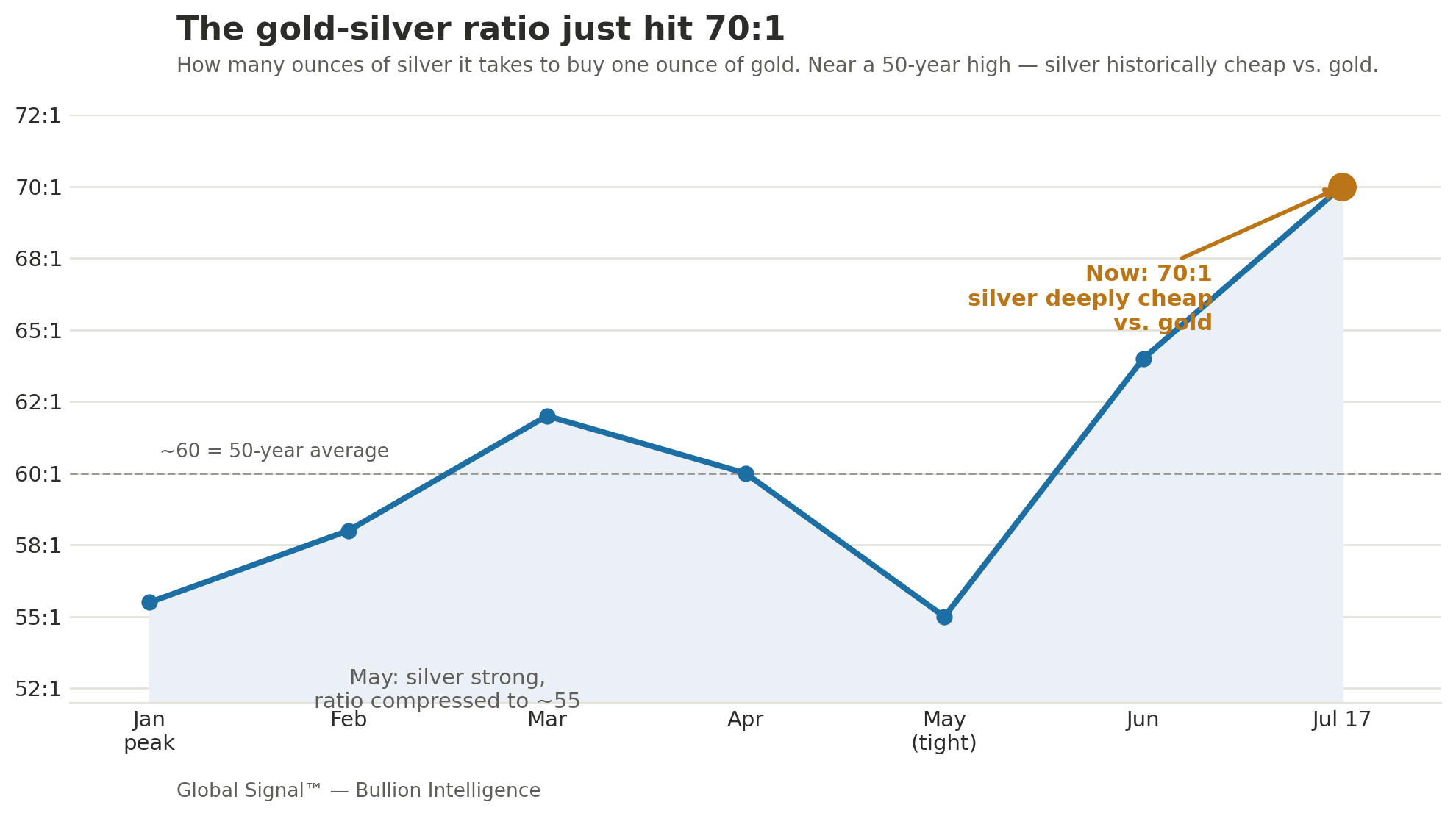

The Picture in One Chart

The chart above shows something worth understanding: the gold-silver ratio, which measures how many ounces of silver it takes to buy one ounce of gold. Back in May, when silver was strong, the ratio was compressed near 55. This week it blew out to 70 — meaning it now takes 70 ounces of silver to buy a single ounce of gold, near the high end of its range over the past fifty years. In plain terms, silver has gotten dramatically cheaper relative to gold. And history says that when this ratio stretches this far, it usually snaps back through silver outperforming — which is the opportunity hiding inside this week’s ugly price action.

Opening Signal

Here’s the heart of it: gold is trapped between good news about the past and bad news about the future, and the future is winning.

The good news about the past is real. June inflation cooled meaningfully, and if that were the whole story, gold would be climbing. Lower inflation means the Fed has less reason to raise rates, which lowers the real return on cash and bonds, which makes gold — that pays no interest — more attractive by comparison. That’s why gold jumped $90 the moment the number came out.

But the bad news about the future is also real, and it’s more powerful right now. The Iran war is escalating again, oil is spiking, and the market knows that today’s expensive oil becomes tomorrow’s expensive inflation. So even as June’s number looked good, traders started pricing in a worse July, kept the odds of a September rate hike alive, and pushed the dollar and bond yields back up — all of which pulled gold back down. The economy also refused to cooperate with the dovish story: retail sales came in solid and jobless claims fell to their lowest in ten weeks, showing the economy hasn’t weakened enough to force the Fed’s hand.

So gold is caught. The past says rates should ease; the future says they might not. Until that tension resolves — until we know whether the oil shock feeds through into sustained inflation or fades — gold is likely to stay range-bound, frustrating everyone. But underneath that frustration, the structural buyers keep accumulating, and silver has gotten cheap enough to be genuinely interesting.

Executive Signal — Premium

Gold rallied on backward-looking good news, then surrendered it to forward-looking bad news — and that mechanism is the whole story. June inflation came in soft on Tuesday (3.5% headline versus 3.8% expected, the steepest monthly drop since April 2020, with core at 2.6%), and gold jumped roughly $90 to about $4,089. But over the following two days it gave nearly all of it back, sliding toward $4,000 by Friday. The reason: the June data measured a month when oil was cheap, while this week’s renewed Iran blockade pushed Brent toward $87, and the market is now pricing the forward inflation that expensive oil implies faster than the Fed can act on last month’s improvement. Gold is trapped between a cooling past and a heating future.

The economy refused to weaken, which kept the rate-hike threat alive. Part of why the rally faded is that the data this week didn’t support the dovish case beyond the inflation print. Retail sales rose 0.2% in June, in line with expectations, and initial jobless claims fell by 8,000 to 208,000 — the lowest in ten weeks and well below expectations. A resilient economy gives the Fed room to stay hawkish if inflation re-accelerates. Markets still expect a hold at the July 29 meeting (odds near 90%), but the September meeting remains genuinely live, and that lingering hike threat is what keeps real yields elevated and gold pressured.

The gold-silver ratio hit 70:1, which is a genuine deep-value signal. Silver fell harder than gold again this week, pushing the ratio that measures their relative price to about 70 — meaning it takes 70 ounces of silver to buy one ounce of gold, near the top of its fifty-year range and well above the long-term average around 60. Silver gets hit twice because 58% of its demand is industrial (solar, semiconductors, EVs, AI data centers), so a hawkish Fed that threatens growth pressures silver’s industrial side on top of the monetary side that also weighs on gold. But history is clear: when this ratio stretches this far, it typically resolves through silver dramatically outperforming gold in the subsequent recovery. This is the tactical opportunity inside the week’s weakness.

China bought gold again, extending a streak that tells you everything about the long game. The People’s Bank of China added 14.93 tonnes of gold in June — its largest single-month purchase since October 2023 — extending its buying streak to twenty consecutive months, and it did this during gold’s worst quarterly decline since 2013. This is a multi-year reserve policy decision, not a reaction to any single data point. While Western traders sold gold on the rate fears, the most strategic buyer on earth kept accumulating. That divergence between the panicking paper market and the patient physical buyer is the defining feature of this entire correction.

The structural case is completely untouched by any of this week’s noise. US federal debt now exceeds $39 trillion with annual interest above $1 trillion, the fiscal backdrop that pushes nations toward gold hasn’t changed, and the institutional price targets remain far above spot — JPMorgan sees $4,800-$6,300 by year-end, Metals Focus targets $4,920. One soft inflation print didn’t make the case, and one faded rally doesn’t break it. The near-term is a rate story caught between oil and the Fed; the multi-year story is a debt-and-dedollarization story that grows stronger regardless.

Key Signals at a Glance — Premium

June inflation came in soft Tuesday (3.5% headline vs 3.8% expected, steepest monthly drop since April 2020; core 2.6%), and gold jumped ~$90 to ~$4,089 — then gave nearly all of it back by Friday, sliding toward $4,000.

The reason: June’s data measured a cheap-oil month, but the renewed Iran blockade pushed Brent toward $87 this week. The market is pricing forward inflation (from expensive oil) faster than the Fed can act on last month’s improvement.

The economy stayed resilient — retail sales +0.2%, jobless claims down to 208K (lowest in 10 weeks) — keeping the September rate-hike threat alive even as a July hold looks near-certain (~90% odds).

The gold-silver ratio hit 70:1, near a 50-year high (average ~60). Silver gets hit twice (58% industrial demand + monetary), but history says extreme ratios resolve through silver outperforming.

China’s PBoC bought 14.93 tonnes in June — largest since October 2023, 20th straight month — during gold’s worst quarter since 2013. The strategic buyer accumulates while Western traders sell.

The structural case is intact: US debt above $39T, interest above $1T/year. JPMorgan targets $4,800-$6,300 by year-end; Metals Focus $4,920; silver targets near $79-81 (implying a ratio back toward 50:1).

The real positioning map starts below →

Conviction map, named vehicles for each thesis, forward scenarios with confidence tiers, the Cycle & Cosmos read, and the Watch Triggers for the weeks ahead — in the Premium Subscription. Premium subscribers see this on publish day. Free subscribers receive it 7 days later.