Gold Got Hit From Both Sides. The Floor Didn’t Move. | Global Signal™ — Bullion Intelligence

Two punches knocked gold to seven-month lows. The same week, a record share of central banks said they're buying.

Last Friday, I told you Thursday’s reversal looked like a bottom — that gold rising on a day of all-bad news smelled like sellers running out of ammunition. I want to start this week by being straight with you: that call was early. The week that followed knocked gold to seven-month lows, and if you bought Thursday’s bounce expecting a clean turn, you’ve felt it. When I get the timing wrong, you’re going to hear it from me plainly, because the alternative — pretending every call lands — is how newsletters lose the people who actually depend on them.

Here’s what happened, and why I think the bigger picture is still very much intact even though the price went the other way.

Gold got hit from two directions at once. First, the good news: the US and Iran reached their peace deal over the weekend and agreed to reopen the Strait of Hormuz, with the signing set for Friday. That’s wonderful for the world — and it pulled the “war premium” right out of gold, the extra safety demand that the conflict had been adding. Then, on Wednesday, the second hit: Kevin Warsh ran his first Federal Reserve meeting as chairman, and instead of the friendly, rate-cutting tone many expected, he came in firm on inflation. Nine of the Fed’s nineteen officials now expect at least one rate increase this year, the Fed raised its inflation forecasts, and the dollar jumped to its highest level in over a year. Higher rates and a stronger dollar are both headwinds for gold, which pays no interest. Take the war premium off with one hand and add a hawkish Fed with the other, and you get what we got: gold sliding to around $4,210, near seven-month lows, down about 22% from its January peak.

So that’s the painful part, told honestly. Now here’s the part the headlines mostly buried, and it’s the reason I’m not the least bit worried about the long-term story.

That very same week, the World Gold Council released its annual survey of the world’s central banks — the people who actually move this market — and a record 45% of them said they plan to buy more gold over the next twelve months. That’s the highest in the survey’s nine-year history. Not one single central bank said it plans to reduce its gold. And 89% expect the world’s total central bank gold holdings to keep rising. The price got knocked down by traders reacting to the news of the day. The institutions that think in decades told us, that exact same week, that they’re still buying. That gap is the whole story.

Opening Signal

Here’s the one thing to hold onto this week: there are two different gold markets, and they’re telling two different stories right now.

The first is the paper market — futures, traders, the daily price on your screen. That market reacts to headlines, and this week the headlines were a peace deal and a hawkish Fed, both of which say “sell gold today.” So it did. The second is the physical market — the central banks, the long-term holders, the people buying real metal and putting it in a vault for twenty years. That market reacts to the deep, slow questions: government debt, currency stability, trust in the dollar. And that market, this week, said it’s buying more than ever.

When those two markets disagree — when the paper price falls while the physical buyers step up — history says the physical buyers are usually the ones to follow. They’re not trading the news. They’re positioning for where this all ends up. The price came down. The floor under it did not move.

Executive Signal

The correction got deeper, and I’m telling you that plainly. Gold fell to around $4,210 this week, near seven-month lows and down roughly 22% from the January peak. Last week’s reversal did not hold, and the cause was a rare double-hit: the peace deal removed the war premium at the same moment Warsh’s first Fed meeting came in hawkish, pushing up the dollar and rate-hike expectations. Both forces pressure gold, and they landed together. If you’ve been holding, this has tested your patience, and there’s no honest way to dress that up.

But the cause of the drop is exactly the kind that’s temporary. The war premium can only come off once — it’s a one-time adjustment, not an ongoing drag. And the hawkish Fed surprise is a single meeting’s tone, not a permanent condition; rate expectations move with the data, and the same peace deal that hurt gold this week should help cool inflation over the coming months, which would eventually ease the rate pressure. Neither of the two things that knocked gold down is a lasting structural change. They’re news-cycle forces, and news cycles turn.

The structural floor was confirmed the same week, and this is the part that matters most. The World Gold Council’s annual central bank survey landed with a record 45% of central banks planning to add gold over the next year, the highest in nine years, with zero planning to cut and 89% expecting global reserves to keep rising. On top of that, 74% expect the dollar’s share of global reserves to fall over the next five years — which is the quiet engine behind all the gold buying. The institutions that actually drive this market told us, at gold’s weakest moment of the year, that their conviction is at a record high.

Silver took the harder hit and offers the bigger opportunity, as usual. Silver got whipsawed violently this week, jumping nearly 3% on the peace deal one morning and then giving it all back when the Fed turned hawkish. It’s the more volatile metal because it’s half industrial, and that volatility cuts both ways. But the structural story is striking: the Silver Institute projects a sixth straight year of supply deficit, and above-ground stockpiles have been drawn down by over 760 million ounces since 2021. A market that tight doesn’t need much of a demand recovery to move sharply, and the reopening of trade as the war ends should help restart the industrial demand that silver runs on.

For the patient holder, this is a deeper discount inside an intact bull market, not a broken thesis. The price is being driven by short-term traders reacting to two temporary forces, while the long-term owners are buying at a record rate. That’s the definition of an opportunity for those who can hold.

Key Signals at a Glance

Gold fell to ~$4,210, near seven-month lows and down ~22% from the January peak, hit by a rare double-whammy: the Iran peace deal removed the war premium, and Warsh’s first Fed meeting came in hawkish.

The Fed held rates at 3.50-3.75% but signaled hike risk — 9 of 19 officials now expect at least one 2026 increase, inflation forecasts were raised, and the dollar surged to its highest since May 2025.

The same week, the World Gold Council’s annual survey showed a record 45% of central banks plan to add gold over the next year (highest in 9 years), zero plan to cut, and 89% expect global reserves to keep rising.

74% of central banks expect the dollar’s share of global reserves to fall over the next five years — the structural engine behind the gold buying. Central banks bought a net 244 tonnes in Q1.

Silver whipsawed — up ~3% on the peace deal, then gave it back on the hawkish Fed. But the Silver Institute projects a 6th straight annual supply deficit; above-ground stockpiles are down 760M+ ounces since 2021.

The peace deal signing is set for Friday in Switzerland. Major banks are holding their targets: Barclays at $4,791, others at $4,900-$6,000, calling the correction a reset, not a reversal.

The real positioning map starts below →

Conviction map, named vehicles for each thesis, forward scenarios with confidence tiers, the Cycle & Cosmos read, and the Watch Triggers for the weeks ahead — in the Premium Subscription. Premium subscribers see this on publish day. Free subscribers receive it 7 days later.

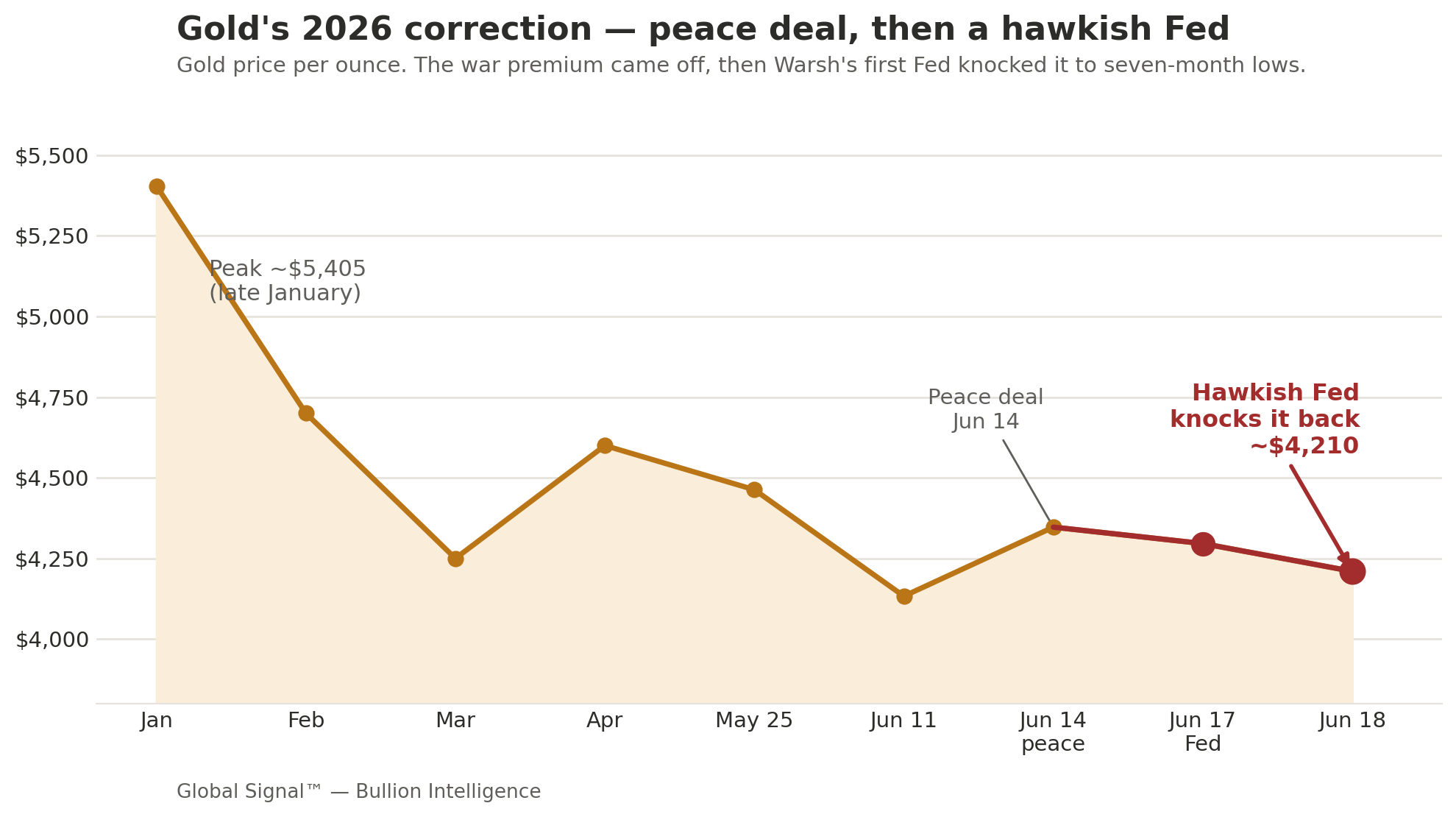

The Picture in One Chart

The chart above shows the whole 2026 journey, and this week’s twist sits right at the end. Gold peaked near $5,405 in January, ground lower through the spring, bounced on that Thursday reversal I wrote about last week — and then ran into the double-whammy. You can see the small bump up around the June 14 peace deal, and then the red slide as Warsh’s hawkish Fed on June 17 knocked it back to about $4,210. Two punches, back to back. What the chart can’t show you is the thing happening underneath it: that same week, a record share of the world’s central banks said they’re buying. The line went down. The buyers underneath it got more committed.

Market Breakdown — Premium

This Week’s Pulse

Gold sits near $4,210-4,300 after a rough week, having fallen nearly 2% on the Fed decision alone to reach seven-month lows. The dollar surged to its highest since May 2025, which is a direct headwind for gold, and shorter-term Treasury yields jumped as the hike odds rose, raising the opportunity cost of holding metal. Silver is the more dramatic chart, whipsawing from a 2.8% morning gain on the peace deal to giving it all back on the Fed, now sitting in the high $60s. The gold-to-silver ratio pushed back up toward 64 as silver fell harder. Oil — the thing that started this whole chain — has dropped sharply toward the low $80s on the peace deal, down about 12% from a week ago, which is the quiet good news that should help inflation cool over the coming months. The peace deal signing is set for Friday, and safe-haven demand has faded as both sides signaled they intend to sign.

Why Gold Got Hit From Both Sides

It’s worth slowing down on the mechanics here, because understanding them is what keeps you calm. Gold had two sources of demand propping it up: the war premium (people buying safety during the conflict) and the structural bid (central banks and long-term holders buying for the deep reasons). This week, the war premium got removed by the peace deal — that’s a one-time event, the premium comes off once and it’s gone. At the same moment, the Fed surprised hawkish, which strengthened the dollar and raised rates, both of which make non-yielding gold less attractive to traders right now. So the two things holding the price up got weaker in the same week, while the structural bid — the part that actually matters long-term — got stronger. The price reflects the short-term forces. The floor reflects the long-term one.

The Warsh Surprise

Markets expected Kevin Warsh to be friendly to lower rates, and his first meeting genuinely surprised people. He held rates steady, as expected, but his tone was firm: “Persistently high prices are a burden for the American people, but the recent past need not be prologue,” he said, emphasizing the Fed’s commitment to price stability. He notably scrapped some of the Fed’s traditional forward guidance, which is a real change in how the Fed communicates. For gold, the immediate effect was negative — a hawkish Fed means higher-for-longer rates and a stronger dollar. But here’s the nuance worth holding: Warsh is reacting to inflation that was largely caused by the war’s oil shock, and that shock is now reversing as the strait reopens. If inflation cools over the coming months the way the falling oil price suggests it should, the hawkish tone has a shelf life.

Macro Undercurrents — Premium

Four forces are working under the surface this week.

The two forces that hit gold are both temporary, which is the key to not panicking. The war premium coming off is a one-time adjustment — it can’t keep subtracting from the price because once it’s gone, it’s gone. The hawkish Fed tone is a single meeting’s stance, and it’s a response to oil-driven inflation that’s now reversing. Neither is a permanent structural change to why gold is valuable. Contrast that with the things holding gold up, which are deep and slow-moving: government debt, currency debasement, central bank diversification. The temporary forces pushed the price down this week; the permanent forces are unchanged. That asymmetry is why I read this as a deeper discount rather than a broken thesis.

The central bank survey is the most important data of the week, and it confirms the floor at gold’s weakest moment. The timing could not be more telling: at the exact moment the paper price hit seven-month lows, the World Gold Council reported that a record 45% of central banks plan to add gold, none plan to cut, and 89% expect global reserves to keep climbing. These are the biggest, most patient buyers in the market, and they don’t trade the daily headlines. When they tell you, at the price low, that their conviction is at a nine-year high, that’s the signal that matters more than any single week’s price action. The survey was conducted partly during the war, so it reflects how reserve managers think when the world feels dangerous — and the answer is: buy more gold.

The dollar’s long-term decline is the engine almost nobody talks about. Buried in that same survey is the number that explains everything: 74% of central banks expect the dollar’s share of global reserves to fall over the next five years. That’s the real reason central banks keep buying gold — they’re slowly, deliberately diversifying away from a dollar-centric system, and gold is the asset they’re moving toward. This week’s dollar spike is a short-term move inside a long-term decline. The central banks are positioning for the long-term decline, not the short-term spike, and that’s why a strong-dollar week doesn’t change their behavior at all.

Silver’s tightening supply is setting up underneath the volatility. While silver got whipsawed on the macro news, the structural story kept quietly building. A sixth straight year of supply deficit, projected at over 46 million ounces, and more than 760 million ounces drawn down from above-ground stockpiles since 2021. This is a market getting physically tighter year after year. The reopening of global trade as the war ends should restart the industrial demand — solar, electronics, manufacturing — that silver depends on. When a market this tight gets a demand recovery, the moves can be sharp, which is the upside case underneath this week’s noise.

Smart Money — Premium

Three institutional patterns define the week.

The central banks confirmed their conviction at the price low, which is the textbook smart-money signal. Buying when the price is weak and others are fearful is precisely what informed, patient capital does, and the survey shows that’s exactly the posture of the world’s central banks right now. A record share planning to add, none planning to cut, at seven-month lows. They’re not reacting to Warsh or the peace deal; they’re executing a multi-year diversification strategy that a hawkish Fed meeting doesn’t dent. When you feel nervous about the price this week, remember that the most sophisticated buyers in the world chose this exact moment to reaffirm they’re buying.

The major banks are holding their high targets through the correction, which tells you how they read it. Barclays held its $4,791 gold target through the 26% correction, and other desks maintain targets in the $4,900 to $6,000 range. Independent research firms — CPM Group, others — are publicly calling this correction a positioning reset rather than a structural reversal. When the analysts who set price targets watch gold fall 22% and keep their targets, they’re telling you they see the drop as temporary and the upside as intact. They could be wrong, but their conviction at these levels is itself information.

Physical demand keeps absorbing the paper-driven dips. The pattern we’ve documented all year held again: every time the paper price falls on a macro headline, physical buyers step in to accumulate. Q1 saw central banks buy 244 tonnes and bar-and-coin demand jump 50% year-over-year even as the price corrected. The paper market sets the daily price; the physical market sets the floor. As long as physical demand keeps meeting these dips, the structural support holds regardless of what the futures traders do day to day.

Conviction Map — Premium

Overweight — physical gold and silver in allocated form, silver-weighted exposure given its deeper discount, gold and silver royalty and streaming names, and quality producers. The deeper correction created a better entry; the record central bank survey confirms the thesis.

Tactical — this is a deeper accumulation zone than last week, and the double-whammy that caused it is temporary. Accumulate in tranches — the $4,200 area is being tested, and a further dip toward $4,000 on continued dollar strength would be a gift for patient buyers, not a warning. Keep dry powder for it.

Underweight — leveraged paper positions that get shaken out exactly at moments like this week, unallocated accounts where you don’t own real metal, and weak miners that can’t endure a prolonged soft patch in the price.

Hedges — physical metal is the hedge against the structural debt and dollar-debasement story that the central bank survey just confirmed is accelerating. Hold the core allocation through the noise, and treat the Fed-driven dollar spike as the short-term move it is.

Portfolio Playbook — Premium

The cleanest expressions of the thesis, grouped by role. The emphasis stays on physical and silver given the deepening discount.

Physical and core exposure:

IAU (iShares Gold Trust) — low-fee core gold exposure, simple to hold in any brokerage account

SIVR (abrdn Physical Silver Shares) — physically-backed silver at a competitive fee, exposure to the deeper discount

PSLV (Sprott Physical Silver Trust) — fully allocated, redeemable physical silver for those who want delivery optionality

Royalty and streaming — the lower-risk way to own miners:

FNV (Franco-Nevada) — the largest, most diversified gold royalty, built to weather soft-price stretches

WPM (Wheaton Precious Metals) — silver-weighted royalty leverage, the cleanest play on a silver recovery and the tightening supply story

RGLD (Royal Gold) — a focused, financially disciplined royalty name

Producers and broad exposure:

AEM (Agnico Eagle) — a premier, low-cost gold producer with a strong balance sheet

PAAS (Pan American Silver) — a quality silver producer with real leverage to a silver repricing

GDX (VanEck Gold Miners ETF) — a diversified basket of major miners for one-ticket exposure

How to use the week: the price got hit by two temporary forces while the permanent forces got stronger, which makes this a better accumulation zone than last week, not a worse one. Buy in tranches, keep powder for a possible dip toward $4,000, and lean silver-heavy given the deeper discount and the tightening supply. The central banks bought the low; patient holders can too.

Cycle & Cosmos — Premium

A Common-Sense Guide for Investors

Let me try something a little different this week, because the timing of what just happened is genuinely uncanny, and it’s worth sitting with.

This week gold got hit from two sides and fell to its lowest in seven months — and in the very same week, the world’s central banks announced their highest conviction to buy gold in nine years. The crowd panicked at the exact moment the wisest, most patient money doubled down. That right there is the oldest pattern in all of markets, and it has a rhythm to it that’s worth understanding, because once you see it, you can’t unsee it.

The pendulum, not the straight line. Most people imagine markets moving in straight lines — up or down. They don’t. They move like a pendulum, swinging from too much fear to too much greed and back again, always overshooting in both directions before returning to the center. Right now the pendulum has swung hard toward fear in the paper gold market: traders dumping on the peace deal and the Fed, pushing the price to an extreme. But here’s what the old-timers know — the further the pendulum swings toward fear, the more energy it stores for the swing back. When you see the price at an extreme low while the smartest buyers are loading up, you’re watching the pendulum reach the end of its arc. It doesn’t stay there. It never stays there.

The tide is still coming in, even when a wave pulls back. We talk a lot in this section about tides, and here’s why it fits: a single wave can retreat down the beach even while the overall tide is rising. This week was a wave pulling back. But the tide — the long, slow, decades-long move of the world’s money out of paper promises and into real assets — is still coming in, and the central bank survey is the clearest tide-gauge we have. A record share of nations moving toward gold, three-quarters of them expecting the dollar to shrink as a share of reserves. That’s not a wave. That’s the tide. Don’t confuse the two, and don’t let a retreating wave convince you the ocean is going out.

The cycle of fear and conviction. There’s a deep cycle that runs underneath every market, older than any chart: the cycle where the many react and the few position. The many react to the news of the day — the peace deal, the Fed, the headlines — and their reaction moves the price around in the short term. The few position for the deep currents — the debt, the dollar, the slow loss of trust in paper money — and their positioning determines where the price ends up over years. This week you got to watch both happen at once, side by side: the many sold gold to seven-month lows, the few told us they’re buying at a record pace. When you can see that split clearly, the question answers itself. Which group do you want to stand with?

Where the clock points. We remain inside that 2025-2027 window where the old debt-based financial order gets tested and real assets reassert their ancient role. This week didn’t change that — if anything, a hawkish Fed fighting war-driven inflation while debt climbs past $37 trillion is the stress in that window playing out in real time. The destination the cycle keeps pointing toward — a reckoning for paper money and a return to the tangible — is exactly what 45% of the world’s central banks just told us they’re preparing for. The price zigzags. The direction holds.

The takeaway. Don’t stand on the beach watching one wave retreat and conclude the ocean has abandoned you. This week was a wave pulling back — two temporary forces knocking the price to a low — while the tide of central bank buying came in at a record pace underneath. The pendulum swung toward fear; it always swings back. If gold is your anchor through the turbulence ahead, a moment when the price is low and the patient money is buying is a moment to quietly add to the anchor, not abandon it. Stand with the few who position, not the many who react.

What to watch right now:

The Friday peace-deal signing — confirms the war premium is fully gone and lets the structural story take over.

Whether oil keeps falling — the key to inflation cooling, which would eventually soften the hawkish Fed pressure.

Whether gold holds the $4,000-$4,200 zone — the level where the physical buyers and central banks have been stepping in.

Forward Scenarios — Premium

Reset-and-recover case — High confidence — The double-whammy marks the bottom of the correction or close to it. The war premium is fully out, oil keeps falling, inflation cools over the coming months, and the hawkish Fed pressure eases as the data improves. Gold bases in the $4,000-$4,300 zone and turns up in the second half as the structural central bank bid reasserts. Silver leads on its supply tightness and the industrial restart. Confirms if: gold holds above $4,000, oil stays down, and the next inflation reading shows the oil shock fading.

Deeper-dip case — Medium confidence — The dollar keeps strengthening on the hawkish Fed, gold tests $4,000 or briefly dips below before the central bank floor catches it. This would be the deepest discount of the cycle and the best entry, not a thesis break, because the record central bank demand and the structural story remain fully intact. Patient buyers with dry powder get rewarded. Confirms if: the dollar pushes higher, gold breaks $4,000 on a fresh Fed or data shock, but physical demand absorbs it.

Extended-pressure case — Speculative — The Fed stays aggressively hawkish, actually hikes later in the year, the dollar runs further, and gold grinds toward $3,800 before finding footing. Even here, the central bank survey and the debt/dollar story don’t change — this would be a generational entry point, not a reason to abandon metal. Confirms if: the Fed signals or delivers a hike, the dollar breaks decisively higher, and gold loses $4,000 with conviction.

Watch Triggers — Premium

The Friday peace-deal signing in Switzerland. Confirms the war premium is fully removed and clears the way for the structural story to drive the price. A stumble would briefly revive safe-haven demand.

Oil’s trajectory. The key to whether inflation cools. Sustained declines toward the $70s would ease the inflation pressure and, in time, soften the hawkish Fed stance that hit gold this week.

Whether gold holds the $4,000-$4,200 zone. The level where central banks and physical buyers have repeatedly stepped in. Holding it confirms the floor; a clean break would open the deeper-dip scenario.

The dollar index. This week’s surge to a one-year high is the immediate headwind. Watch whether it extends or rolls over — a softening dollar is the catalyst that would let gold’s structural bid reassert.

Central bank buying data and follow-through on the survey. The record 45% intending to buy is the structural anchor. Watch the monthly purchase data for confirmation that intent is becoming action.

TL;DR — Premium

I told you last Friday that Thursday’s reversal looked like a bottom — that was early, and this week proved it. Gold got hit from both sides: the Iran peace deal removed the war premium, and Warsh’s first Fed meeting came in hawkish (9 of 19 officials now expect a 2026 hike, the dollar hit a one-year high), knocking gold to ~$4,210, near seven-month lows and down 22% from the peak.

But both forces are temporary — the war premium comes off only once, and the hawkish tone is a response to oil-driven inflation that’s now reversing. And the structural floor was confirmed the same week: the World Gold Council’s survey showed a record 45% of central banks plan to add gold, none plan to cut, 89% expect global reserves to rise, and 74% expect the dollar’s reserve share to fall. The crowd sold to seven-month lows; the patient money announced record conviction.

Positioning stays overweight physical and quality miners — royalty (FNV, WPM, RGLD), producers (AEM, PAAS, GDX), physical (IAU, SIVR, PSLV) — silver-weighted given the deeper discount and a 6th straight supply deficit. Accumulate in tranches, keep powder for a possible dip toward $4,000. The Cycle & Cosmos read: a single wave pulled back while the tide came in underneath. The pendulum swung to fear; it always swings back. Stand with the few who position, not the many who react.

— Written by The Global Signal Team

Global Signal™ is published for informational and educational purposes only. Nothing in this newsletter constitutes financial, investment, legal, or tax advice, nor a recommendation to buy, sell, or hold any security, asset, or strategy. The Cycle & Cosmos section is offered as interpretive and educational commentary only and makes no claim of causative effect on markets. All opinions are those of the author at the time of publication and are subject to change without notice. Markets involve risk, including possible loss of principal. Past performance is not indicative of future results. No client or advisory relationship is formed by reading this newsletter. Readers are solely responsible for their own decisions and should conduct independent research and consult a licensed professional before acting on any information. The author and publisher disclaim any liability for losses incurred based on this content. Full terms: https://globalsignalhq.substack.com/tos · © Global Signal™